Bankruptcy Attorneys in Louisville, KY

The Path to Financial Freedom Starts Here With Our Bankruptcy Attorney in Louisville

Are you drowning in debt with no clear way out? Facing relentless harassing phone calls from creditors, sleepless nights, and the crushing burden of financial stress?

You’re not alone. Thousands of Louisville residents find themselves overwhelmed by debt each year, unsure where to turn. O’Bryan Law Offices understands your struggle.

For decades, our experienced bankruptcy lawyers have been helping Kentucky residents regain their financial foundation through strategic bankruptcy filings and debt relief solutions.

Don’t let debt control your life for another day. Let us help you get back on your feet.

📞Contact us today at (502) 339-0222 for a free consultation with an experienced Louisville team member who will listen to your story with compassionate care and guide you to the right place for relief.

Understanding Bankruptcy in Louisville, KY

Bankruptcy is a legal process designed under the bankruptcy code to help individuals and businesses eliminate or repay debt under the protection of federal bankruptcy court. In Kentucky, bankruptcy offers a legitimate, structured pathway to financial recovery for those struggling with debt.

Many people misunderstand bankruptcy, viewing it as a personal failure rather than what it truly is—a legal right provided by federal law to help citizens escape crushing debt and achieve a fresh start. The stigma surrounding bankruptcy often prevents people from exploring this option until their financial situation becomes dire.

The bankruptcy process in Louisville is governed by the United States Bankruptcy Court for the Western District of KY. This federal court oversees all bankruptcy filings in our region and ensures that debtors and creditors are treated fairly throughout the process.

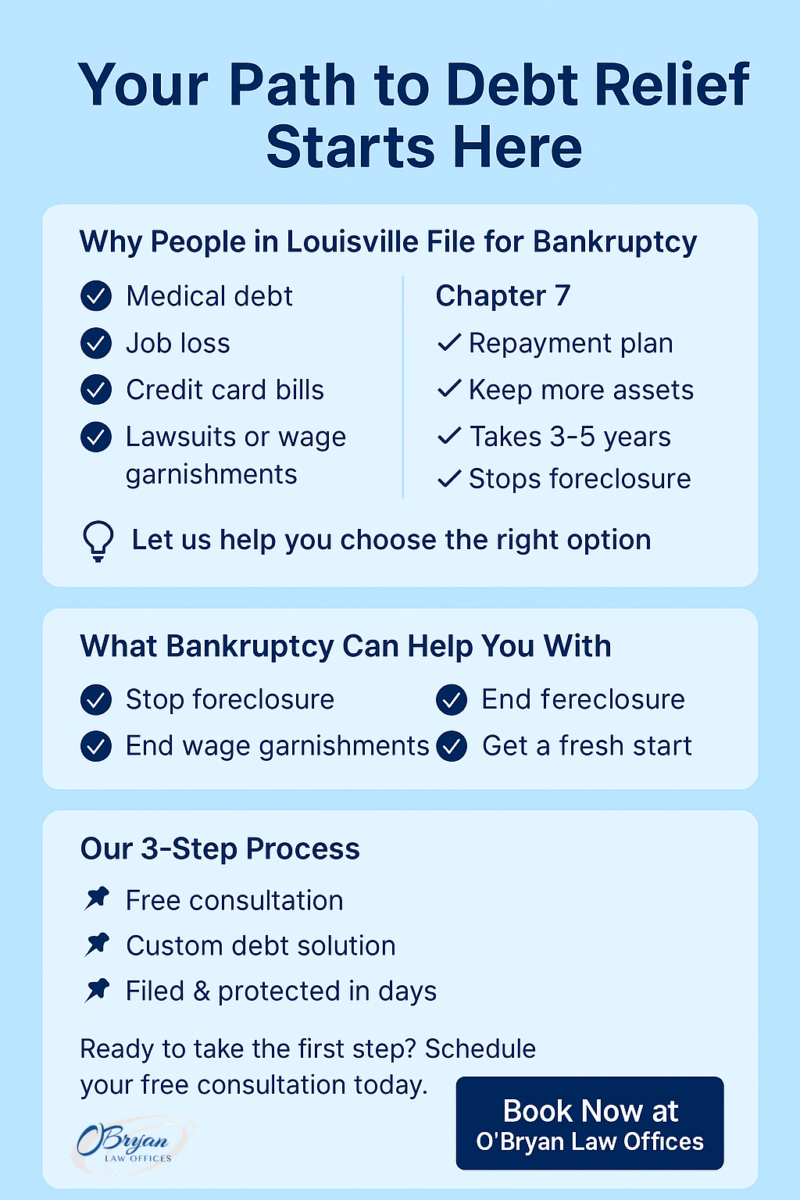

What bankruptcy can and cannot do ⚖️

What it can do:

- Stop foreclosure and repossession

- End wage garnishments

- Eliminate credit card and medical debt

- Stop creditor harassment

- Discharge certain old tax debts

What it can’t do:

- Get rid of liens

- Eliminate child support or alimony

- Wipe out most student loans (except in rare cases)

- Remove recent tax obligations or court fines

Why Choose Our Louisville Bankruptcy Law Firm?

- Over 30,000 families helped

- Board-certified in consumer bankruptcy law

- Offices in Louisville and New Albany

- Fast, compassionate support—you’ll speak with an experienced team member

- Clear, honest advice on every option—not just bankruptcy

Our proven process helps you Restart. Rebuild. Restore. ✨

Types of Bankruptcy: Chapter 7 vs. Chapter 13

Understanding the different types of bankruptcy is important when determining which option best suits your financial situation.

| Feature | Chapter 7 (Liquidation) | Chapter 13 (Reorganization) |

|---|---|---|

| Duration | 3–4 months | 3–5 years |

| Income Requirement | Must pass a means test | Must have regular income |

| Debt Discharge | Most unsecured debt wiped out | Partial repayment, remaining debt discharged after plan |

| Property Risk | Non-exempt assets may be sold | Keep all property while repaying |

| Stops Foreclosure? | Temporarily | Yes, allows repayment |

| Co-Signer Protection | No | Yes (co-debtor stay) |

| Credit Report Duration | Stays on for 10 years | Stays on for 7 years |

Chapter 7 bankruptcy, often called “liquidation bankruptcy,” allows you to eliminate most unsecured debts within 3-4 months. In this process, a court-appointed trustee may sell certain non-exempt assets to pay creditors, though most Louisville filers can protect their essential property through state and federal exemptions.

To qualify for Chapter 7 bankruptcy, you must pass a “means test” that evaluates your income relative to the Kentucky median for your household size.

Chapter 13 bankruptcy, known as “reorganization bankruptcy,” creates a 3-5 year repayment plan that allows you to keep your property while paying off a portion of your debts. This option is particularly beneficial for homeowners facing foreclosure, as it can stop the process and provide time to catch up on mortgage payments.

Chapter 13 bankruptcy is suitable for those with regular income who exceed the Chapter 7 means test thresholds.

Contact us today! O’Bryan Law Offices have over 40 years of experience helping clients determine if a Chapter 7 or Chapter 13 bankruptcy is right for their situation, providing relief tailored to each client’s unique circumstances.

Debts Dischargeable Through Bankruptcy

One of the most significant benefits of filing for bankruptcy is the discharge of debts, which legally eliminates your obligation to repay specific financial obligations.

Bankruptcy can typically eliminate unsecured debts such as credit card debt, medical bills, personal loans, utility bills, and certain older tax obligations. These common bills often make up a substantial portion of what overwhelms Louisville residents, and their discharge can provide immediate debt relief and a fresh start.

However, certain debts cannot be discharged through bankruptcy, including child support, alimony, recent tax debts, student loans (except in rare cases of proven hardship), court-ordered fines, and debts resulting from fraud.

If you have co-signers on any of your loans, they may still be responsible for the debt even after your bankruptcy discharge unless they file themselves.

Protecting Your Assets: Exempt and Non-Exempt Property

A common concern for those considering bankruptcy is whether they’ll lose their home, car, and personal belongings in the process. Kentucky law provides specific exemptions that allow you to protect essential assets during bankruptcy.

In Kentucky, homeowners can exempt up to $31,575 of equity in their primary residence. This means that if your home equity falls within this limit, you can typically keep your home during bankruptcy.

Kentucky law also allows you to exempt up to $5,000 for a vehicle, retirement accounts, household items, and tools needed for your occupation, subject to specific limits.

The bankruptcy trustee’s role is to review your assets and determine what property might be non-exempt. With proper planning and exemption strategies, most Louisville bankruptcy filers can protect their essential property.

At O’Bryan Law Offices, we work diligently to maximize your exemptions, ensuring you keep as many assets as legally possible while still obtaining relief from your debts.

Impact of Bankruptcy on Credit and Future Financial Opportunities

While bankruptcy provides immediate relief, it impacts your credit and future financial options.

A Chapter 7 bankruptcy typically remains on your credit report for 10 years, while Chapter 13 stays for 7 years. Initially, your credit score will likely decrease, but many clients begin seeing improvement within 12-24 months after filing, especially if they had already fallen behind on payments before bankruptcy.

Rebuilding credit after bankruptcy is entirely possible and follows a predictable path. Many O’Bryan Law Offices clients qualify for secured credit cards within months of discharge, auto loans within 1-2 years (albeit at higher interest rates initially), and can even qualify for mortgages within 2-4 years after bankruptcy, depending on their financial recovery.

While some employers in financial sectors may consider bankruptcy in hiring decisions, federal law prohibits employers from firing you solely because you filed for bankruptcy. Many clients find that the reduced financial stress and elimination of wage garnishment actually improves their work performance and career prospects.

Exploring Alternatives to Bankruptcy

Before committing to bankruptcy, it’s wise to consider all available debt relief options to ensure you’re making the best choice for your specific situation.

Debt consolidation combines multiple debts into a single loan, potentially lowering your interest rate and monthly payment. This approach works best if you have good credit and can qualify for favorable terms. However, it doesn’t reduce the principal amount owed and may not provide sufficient relief for those with substantial debt.

Debt negotiation involves working directly with creditors to reduce balances or interest rates. While this can be effective for some debts, it typically requires lump-sum payments and may result in taxable forgiven debt. Additionally, creditors are not obligated to negotiate, making results unpredictable.

Debt management plans offered through a credit counseling agency can provide structured repayment with reduced interest rates. These plans typically require 3-5 years of consistent payments and may not include all types of debt.

While these alternatives can work in certain circumstances, they often fall short for those with significant debt or when creditors are already pursuing collection actions.

At O’Bryan Law Offices, our Louisville bankruptcy attorneys provide honest assessments of all options, recommending bankruptcy only when it truly represents the most effective path to financial recovery.

Need immediate help with overwhelming debt? Call our phone number at (502) 339-0222 for a free consultation with our experienced team.

Costs Associated with Filing for Bankruptcy

Court filing fees in Kentucky currently stand at:

- Chapter 7: $338

- Chapter 13: $313

Attorney fees vary based on the complexity of your case, but typically range from $1,500 to $2,500 for Chapter 7 and $4,500 to $4,750 for Chapter 13. Additional costs may include credit counseling courses (approximately $15) and credit report fees.

While these costs may seem substantial when you’re already facing financial hardship, they represent a fraction of what most people save through debt discharge.

For those unable to pay upfront, O’Bryan Law Offices offers payment plans that make bankruptcy protection accessible to those who need it most.

| Expense | Chapter 7 | Chapter 13 |

|---|---|---|

| Court Filing Fee | $338 | $313 |

| Attorney Fees (Typical Range) | $1,500 – $2,500 | $4,500 – $4,750 |

| Credit Counseling Courses | ~$15 | ~$15 |

| Payment Plans Available? | Yes | Yes |

Automatic Stay: Halting Creditor Actions

One of the most immediate benefits of filing for bankruptcy is the automatic stay, which takes effect the moment your case is filed with the court.

The automatic stay is a powerful legal injunction that prohibits creditors from continuing collection activities against you. This means an immediate end to:

- Harassing phone calls

- Wage garnishment

- Foreclosure proceedings

- Repossessions

- Utility disconnections

This protection gives you breathing room to work through the bankruptcy process without the constant pressure of creditor actions.

The automatic stay typically remains in effect throughout your bankruptcy case, which may last 3-4 months for Chapter 7 or 3-5 years for Chapter 13. However, creditors can request the court to lift the stay in certain circumstances, such as when a secured creditor seeks to repossess collateral that isn’t being paid for during the bankruptcy.

Our experienced bankruptcy attorneys understand how valuable this immediate relief is for our clients. We prepare and file your bankruptcy petition promptly to ensure you receive the protection of the automatic stay as quickly as possible, often stopping garnishment of your paycheck just days after you retain our services.

Co-Signers and Bankruptcy Implications

When you file for bankruptcy, it’s crucial to understand how your decision might affect those who have co-signed loans with you.

In Chapter 7 bankruptcy, while your personal liability for debts is discharged, your co-signers remain fully responsible for repaying the debt. This means creditors can—and typically will—pursue co-signers for the full amount once your bankruptcy protection is in place. This can strain relationships and place unexpected financial burdens on family members or friends who helped you by co-signing.

Chapter 13 bankruptcy offers more protection for co-signers through what’s called the “co-debtor stay,” which prevents creditors from pursuing co-signers while your repayment plan is in effect, as long as you continue making payments on that debt through your plan. This makes Chapter 13 bankruptcy a more considerate option when co-signers are involved.

We help you through these sensitive situations by developing strategies that minimize the impact on co-signers while still providing you with the debt relief you deserve. This might include:

- Reaffirming specific debts

- Structuring your Chapter 13 plan to fully pay certain co-signed obligations

- Exploring non-bankruptcy alternatives for particular debts

Reach out to our understanding team today for a free consultation so we can discuss your next steps.

Duration of the Bankruptcy Process

Knowing the timeline for bankruptcy helps you plan effectively and set realistic expectations for your financial recovery. Chapter 7 and Chapter 13 bankruptcy follow different timelines.

Chapter 7 typically takes 3-4 months from filing to discharge. The process begins with filing your petition, followed by a creditors’ meeting about a month later. Assuming no complications arise, you can expect to receive your discharge approximately 60-90 days after the creditors’ meeting, at which point most of your debts are legally eliminated.

Chapter 13 bankruptcy follows a longer timeline, lasting 3-5 years, depending on your income and the terms of your repayment plan.

After filing, you’ll begin making payments to the trustee within 30 days, even before your plan is officially confirmed by the court. The confirmation hearing typically occurs 1-3 months after filing. Once all plan payments are completed, you’ll receive a discharge of remaining eligible debts.

Several factors can affect these timelines, including:

- Objections from creditors

- Trustee requests for additional information

- Amendments to your filing

We prepare thoroughly to minimize delays and guide you through each phase of the bankruptcy process in detail, keeping you informed about what to expect next.

Employment Considerations Related to Bankruptcy

Many clients worry about how bankruptcy might affect their current job or future employment prospects.

Federal law provides important protections for bankruptcy filers.

Section 525 of the Bankruptcy Code explicitly prohibits employers from firing you, denying you a promotion, or otherwise discriminating against you solely because you filed for bankruptcy. This protection applies to both government and private employers.

Regarding future employment, government employers cannot consider bankruptcy in hiring decisions. Private employers have more leeway, particularly for positions involving financial responsibility, but many focus more on your current financial stability than past challenges.

In practice, most O’Bryan Law Offices clients report that bankruptcy has little to no negative impact on their careers.

While some employers request credit checks as part of their hiring process, particularly in the financial sector, bankruptcy often proves less problematic than ongoing delinquencies, collections, and high debt-to-income ratios. By resolving your debt issues through bankruptcy, you may actually become more employable in the long run.

Contact Our Louisville Bankruptcy Lawyer Today For a Free Consultation

Taking the first step toward financial freedom can be intimidating, but you don’t have to face it alone. With over 40 years of combined experience, O’Bryan Law Offices provides competent representation through every step of the filing process.

Our Louisville bankruptcy law firm will evaluate your unique financial situation, explain all available options, and help you determine whether bankruptcy is the right choice for you. During your free consultation, we’ll answer your questions, address your concerns, and provide a clear roadmap for moving forward.

With offices in Louisville and New Albany, our bankruptcy law firm serves clients throughout Kentucky and Southern Indiana. Call us today at (502) 339-0222 to schedule your confidential consultation, or visit our Louisville bankruptcy team at 1717 Alliant Avenue, Suite 17, Louisville, KY 40299.

The sooner you reach out, the sooner we can help you stop creditor harassment, prevent foreclosure, and begin your journey toward a debt-free future with the peace of mind you’ve been seeking.

FAQs About Bankruptcy in Kentucky

In most cases, no. Kentucky bankruptcy exemptions allow you to protect up to $31,575 in home equity. Even if you have more equity than the exemption allows, Chapter 13 bankruptcy provides a way to keep your home while catching up on mortgage payments through a structured repayment plan. Our attorneys carefully analyze your situation to develop a strategy that protects your home.

Yes. The automatic stay that goes into effect immediately upon filing bankruptcy stops all wage garnishment. For garnishments already in progress, we can often help recover a portion of wages garnished in the 90 days before filing. After discharge, those debts are typically eliminated, preventing future garnishments.

Bankruptcy will initially lower your credit score and remain on your credit report for 7-10 years. However, most O’Bryan Law Offices clients see their scores begin to improve within 12-24 months after discharge as they establish new credit and build payment history without the burden of overwhelming debt. Many qualify for mortgages within 2-4 years after bankruptcy.

Most unsecured debts can be discharged, including credit card debt, medical bills, personal loans, utility bills, and certain older tax obligations. Non-dischargeable debts include child support, alimony, recent taxes, student loans (except in rare hardship cases), court fines, and debts from fraud. Our team will review your debts to determine exactly what can be eliminated through bankruptcy.

Qualification for Chapter 7 bankruptcy is primarily determined by the “means test,” which compares your average monthly income for the past six months to the median income for a household of your size in Kentucky. If your income falls below the median, you automatically qualify. If it exceeds the median, a more detailed analysis of your disposable income determines eligibility. During your consultation, we’ll perform this analysis and explain your options.

Yes, we provide legal services for both bankruptcy and divorce matters. In fact, these areas often overlap, as financial strain can be both a cause and effect of divorce proceedings. Our experienced lawyers can help you navigate the complexities when bankruptcy and divorce issues intersect, ensuring your rights are protected in both areas of law.