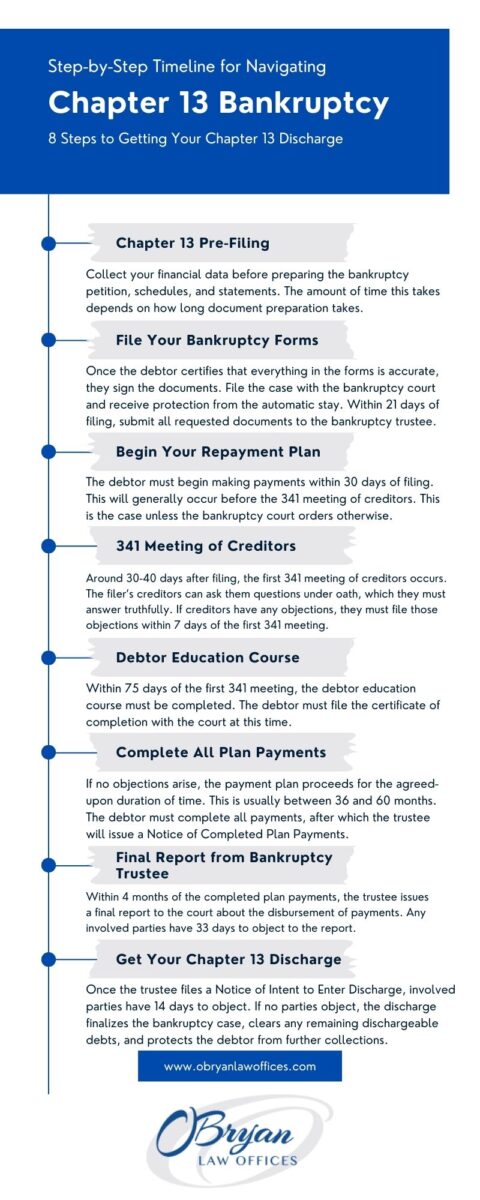

Chapter 13 Closing Process

The final stretch of your bankruptcy case will be handled largely by the bankruptcy trustee, as they must submit certain documents to the court. Usually, the closing process begins after you have completed all of your plan payments, which is around 36-61 months after filing.

Final Report from Bankruptcy Trustee

The trustee must then submit their final report to the court, generally within 4 months of the completion of the repayment plan. This report will inform the court of how the payments were disbursed to your creditors. Concerned parties have 33 days to object to the final report. If nobody objects, the final report is approved by the court.

Notice of Intent to Enter Discharge

After the final report is approved by the court and the debtor has certified certain information, the court will issue a Notice of Intent to Enter Discharge to all concerned parties. This notice informs the parties that the court is preparing to grant your bankruptcy discharge. Concerned parties have 14 days to object to the discharge.

Chapter 13 Bankruptcy Discharge

If no parties object, your Chapter 13 discharge will be granted. A bankruptcy discharge is a decree by the court that prevents creditors from attempting to collect on discharged debts. Think of discharged debts as forgiven debts that you are no longer responsible for paying. Most forms of unsecured debt are dischargeable through bankruptcy.

However, certain debts are not eligible for discharge through bankruptcy, not even through a hardship discharge. Nondischargeable debts include the following.

- Domestic support obligations such as alimony and child support

- Criminal fines and restitution payments

- Certain student loans

- Certain tax debts

Final Decree of the Bankruptcy Case

Around 14 days after you receive your discharge, the court will enter the final decree of the case. This decree officially closes the bankruptcy case and discharges the trustee from their responsibilities in the case.

How Do I Know When My Chapter 13 Is Over?

Your Chapter 13 bankruptcy case is officially, completely over once the court issues the final decree. You will be nearing the end of your case when you complete your repayment plan, submit your final paperwork, and receive your discharge order. Once these are completed, all that remains is receiving the final decree from the court.

Contact a Chapter 13 Lawyer in Kentucky with O’Bryan Law Offices

If your unsecured and secured debts are piling up, bankruptcy can give you the breathing room you need to repay them at a comfortable pace. With the protection of the automatic stay that bankruptcy provides, your creditors can no longer attempt collection efforts against you. This means you can save your house, save your car, stop wage garnishment, and much more. To learn more about how bankruptcy can benefit your situation, please contact the O’Bryan Law Offices today. Call our office at 502-339-0222 today to schedule a free consultation.